How Foreign Buyers Can Buy a Home in France: Legal Process, Costs, and Taxes

Buying a home in France remains one of the most structured and legally secure real estate transactions available to foreign buyers in Europe. Whether the objective is a second home, a primary residence, or a long-term investment, France offers a transparent legal framework, regulated notarial oversight, and strong buyer protections.

This guide explains, step by step, what non-resident buyers need to know in 2026: how the purchase process works, which costs and taxes apply, how financing is handled, and how buying a home differs from buying property purely for investment.

1. Why Buying a Home in France Attracts International Buyers

Yes. There are no legal restrictions on foreign nationals purchasing residential property in France. Non-residents enjoy the same ownership rights as French citizens, regardless of nationality or country of residence.

Key points:

Freehold ownership is permitted

No residency or visa requirement to purchase

Property rights are protected by the French civil code and notarial system

2.Home vs Investment Property in France: Is There a Difference?

France consistently ranks among the most attractive real estate markets in Europe due to:

Regulated purchase process supervised by an independent notaire

Long-term capital preservation characteristics

Political and legal stability

3.What Does “Buying a Home in France” Mean for Foreign Buyers?

For non-residents, buying a home in France can refer to different use cases:

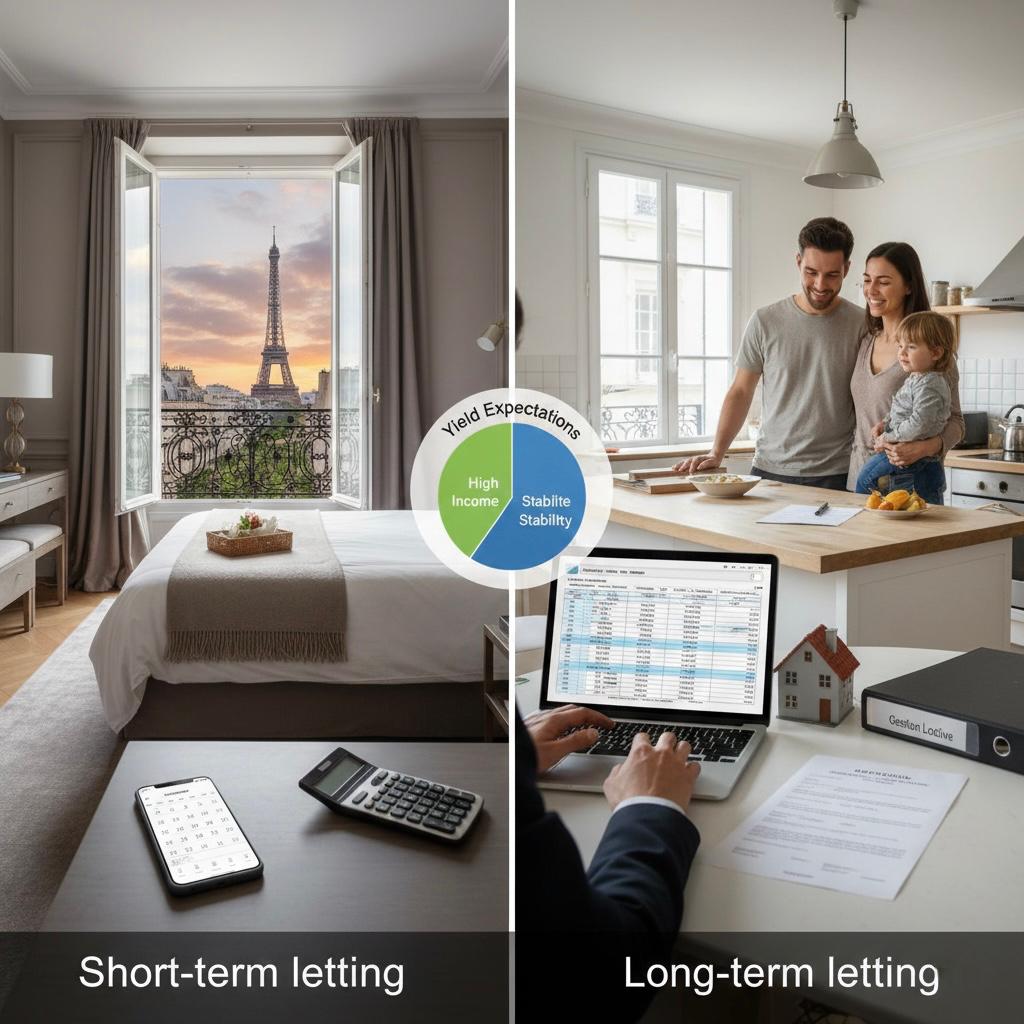

Primary residence (less common for non-residents) Second home for personal use

Mixed-use property (personal use + rental) Pure investment asset

Legally, these uses follow the same acquisition process. The differences arise later in taxation, financing terms, and rental regulation.

4. Buying a Home vs. Buying Property for Investment in France)

When foreign buyers consider purchasing real estate in France, the distinction between buying a home and buying property purely for investment is primarily functional rather than legal. In both cases, the acquisition process, ownership rights, and notarial procedures are identical. French law does not differentiate between a residential home and an investment asset at the point of purchase.

The difference emerges after completion, particularly in intended use and financial strategy. Buying a home is typically driven by personal occupancy, seasonal use, or a mixed personal–rental approach. As a result, financing decisions tend to focus on affordability, long-term holding, and lifestyle considerations rather than short-term yield optimisation.

By contrast, an investment-focused purchase is structured around rental income and capital performance. Tax planning plays a more central role, with greater attention given to deductible expenses, depreciation mechanisms where applicable, and long-term exit taxation. Financing strategies are usually yield-driven, and investors are more sensitive to rental regulation, vacancy risk, and operating efficiency.

In practical terms, while the legal framework remains the same, the tax treatment, financing logic, and risk assessment differ depending on whether the property is acquired as a personal home or as a dedicated investment asset. Foreign buyers should therefore clarify their primary objective before purchasing, as this decision directly affects structuring, tax exposure, and long-term returns.

5. Ways to Buy a Home in France

1. Resale (Existing Property)

Pros

Prime locations and established neighbourhoods

Immediate occupancy or rental potential

Cons

Higher acquisition costs (typically ~7–8%)

Possible renovation and maintenance needs

2. New Build (VEFA / Off-Plan)

Pros

Reduced notary and registration costs (≈2–3%)

Structural guarantees (10-year warranty)

Modern energy standards

Cons

VAT (20%) typically included in price

Delivery and developer risk

3. Renovation / Value-Add Purchase

Pros

Higher capital appreciation potential

Tax mechanisms may offset renovation costs

Cons

Project management complexity

Permit, timing, and budget risk

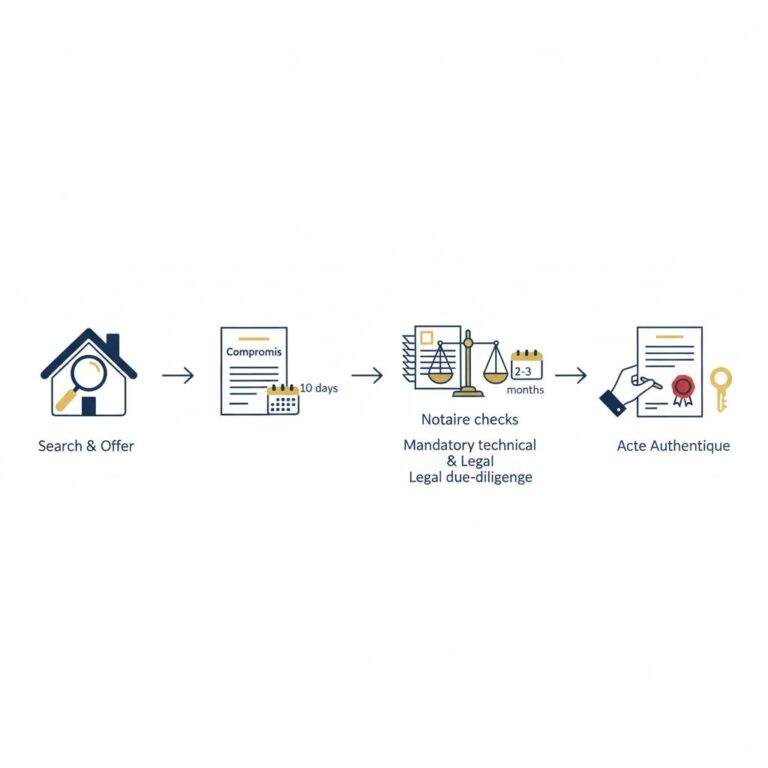

6. The Property Purchase Process in France (Timeline)

No. Purchasing property in France does not automatically grant residency rights. Residency requires a separate visa or residence permit based on specific legal criteria.

There is no legal minimum, but practical entry budgets typically start around €150,000–€200,000, depending on location, property type, and acquisition costs.

On average, the process takes 8 to 12 weeks from the signing of the preliminary contract to final completion at the notary’s office.

Conclusion

Buying property in France as a non-resident is legally straightforward but requires disciplined preparation. Understanding the purchase process, true acquisition costs, taxation, and ongoing obligations is essential to avoiding risk and achieving long-term objectives.

With a transparent legal system, regulated transactions, and diverse real estate markets, France remains a highly reliable destination for international home buyers. Partnering with experienced, France-based professionals such as Home France allows foreign buyers to navigate the market confidently and make informed, compliant decisions aligned with their goals.